In this article, we examine the newly approved MiCA regulation, explain who and what it will cover, and evaluate its effect on the crypto industry in the European market.

The Markets in Crypto-Assets Regulation (MiCAR) was approved by the European Council in April and ratified in May by the EU’s Economic and Financial Affairs Council. Applauded by many for finally bringing regulatory clarity to the EU member states, MiCA introduces a unique and comprehensive regulatory environment to the EU.

MiCA aims to provide certainty in the regulation of crypto-assets not already covered by existing regulations, to set clear rules for crypto-asset service providers (CASPs) and token issuers, and to replace individual member state regulations of the industry with a unifying and comprehensive framework. This means that the European crypto industry will finally get regulative clarity and clear expectations from legislative authorities on how to conduct their business in accordance with EU law.

So, who and what’s covered by MiCA?

At its most basic, MiCA applies to CASPs and crypto-assets operating in the EU or specifically targeting EU investors. CASPs can be:

- Custodial wallets

- Exchanges

- Crypto-asset trading platforms

- Crypto-asset advisers and portfolio managers

MiCA designates three types of crypto-assets that are covered by the legislation. It covers:

- Asset-referenced tokens((like stables backed by commodities) ARTs)

- E-money tokens ((stables backed by a single currency)EMTs)

- Other tokens (like utility tokens)

NFTs are not classified as their own crypto-asset type in the regulation and, as such, are only covered by MiCA to the extent that the particular project or collection can be classified as a utility token. Interestingly, MiCA does not consider all NFTs non-fungible, and assigning a unique identifier to a crypto-asset will not necessarily mean that the asset will be considered non-fungible in a legal sense. For example, NFTs issued in extensive collections with little or no difference in traits and utility may very well fall under MiCA if they can be considered utility tokens or financial instruments.

Crypto-assets that are classified as financial instruments per MiFID II (2014) will, of course, also not be regulated by MiCA. This includes deposits, funds (that do not qualify as e-money tokens), securitization positions, insurance products, and pension products. Moreover, tokens that qualify as transferable securities will also not be subject to MiCAR.

Key Takeaways from MiCA

Fewer Licenses for More Markets!

After the implementation of MiCA, national Web3 permits will be a thing of the past in the European Union. CASPS authorized in their registered country will be able to operate in all EU member states, giving them access to the entirety of the single market.

Higher demands for CASPs!

MiCA places new demands on CASPS to ensure safe and ethical conduct. For example, CASPS will be obligated to:

- Have an office in an EU country and at least one director-resident of the country

- Acting honestly, fairly, and professionally

- Adhere to EU rules on marketing communication

- Follow certain practices to prevent market abuse and handle complaints correctly

- Be public regarding pricing, cost and fee policies, and the environmental impact of the services they provide

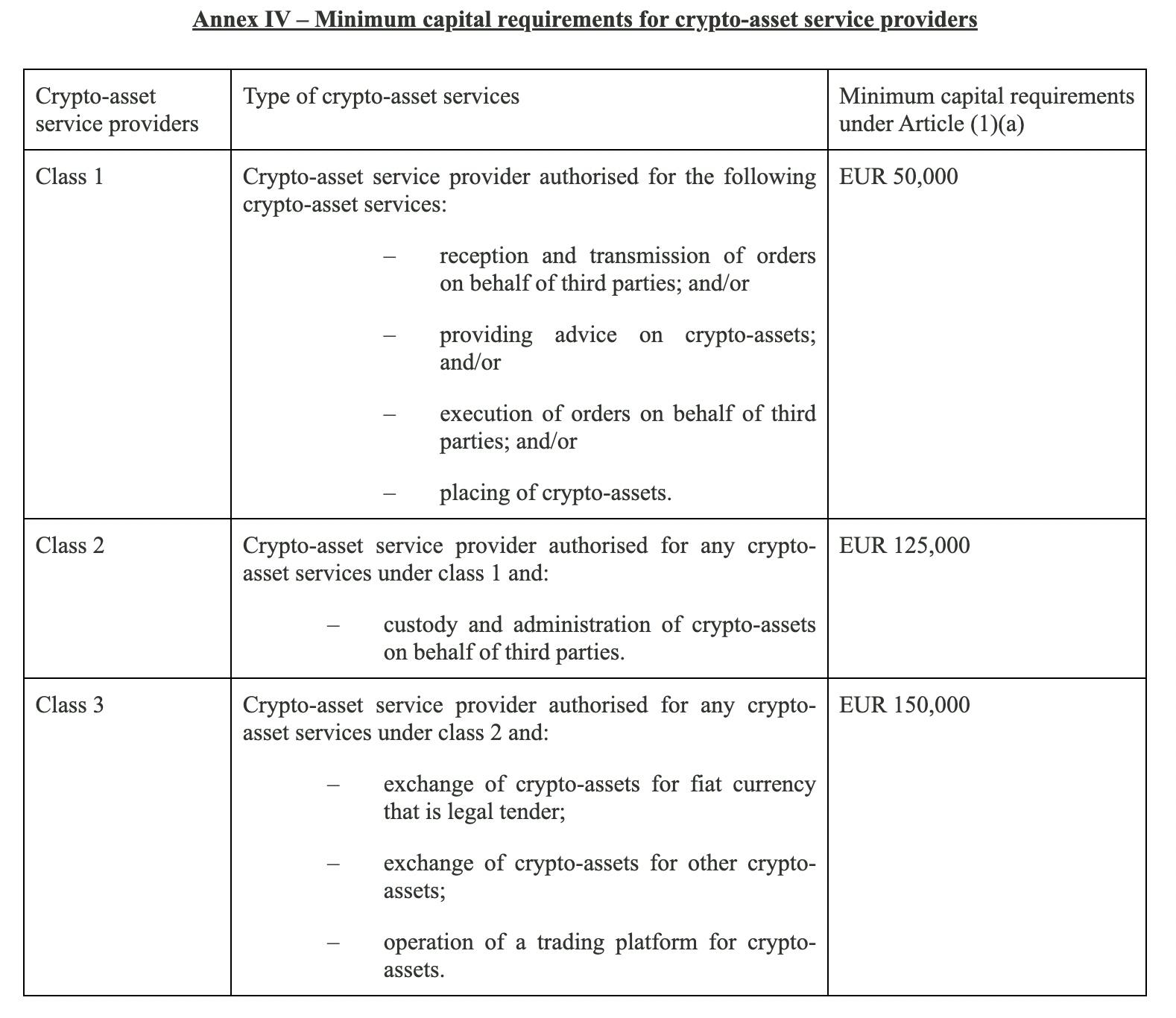

Moreover, new capital requirements for CASPS will also be introduced, as per table 1 below.

Higher standards for token issuance

MiCA also introduces rules for the issuance of crypto-assets. Specifically, it’ll be required to publish a whitepaper and designate a legal entity responsible for the issuance and operation of the project. This means no more undoxxed teams in the EU.

Smaller token offerings (below €1 million within a twelve-month period) may be exempt from this requirement, though. For tokens that do not have an issuer, like BTC, the exchanges that facilitate the trade of the token will bear the responsibility of it.

MiCA also introduces minimum content demands for whitepapers for asset-referenced tokens, e-money tokens, and other tokens.

No More Algocoins!

MiCA makes algorithmic stablecoins a thing of the past. Moreover, MiCA places several new demands for fiat-backed stablecoins, contributing to more security and less volatility.

1. Fiat-backed stablecoins must have a liquid reserve of 1:1

2. Fiat-backed stablecoins must implement certain procedures to safeguard the backing and reserve assets

3. Issuers must establish proper procedures for complaints, and the prevention of market abuse and insider trading

4. Issuers must have a reserve of assets insulated from the rest of their portfolio and held by a third party

So, what does this mean for the European Crypto Market?

Most importantly, MiCA signifies clear regulatory boundaries for the entire industry. For CASPs and token issuers, this means a clear framework to operate in, making it easier to conduct business and raise funds. For investors, the new demands placed on CASPs and token issuers mean a safer environment to invest in and more stable service providers. For token issuers, the minimum content demands mean that whitepapers will have to be more thorough and that undoxxed teams in the EU are a thing of the past.

The supranational license system will make it easier for CASPs and token issuers to operate across EU member states since they only need one license for the entire market instead of 27. The higher demands placed on CASPs by the legislation should result in more transparent, stable, and secure vendors since they’ll have to conform to EU legislation on marketing communications, be transparent regarding their cost structure, and keep a sizable amount of capital ready at hand.